What is a Demand Letter?

Get a Free Consultation

A demand letter is a critical document in the realm of personal injury law. It serves as the initial step in negotiating with insurance companies, laying the groundwork for a successful claim.

While our personal injury law firm is in Tampa, Florida, we serve clients throughout the state. We have written thousands of demand letters resulting in the collection of millions of dollars for our clients, so we know how to write demand letters and their importance.

A well-written and well-supported demand letter, complete with the appropriate records, can play a pivotal role in resolving a personal injury claim expeditiously.

It serves as a comprehensive presentation of your case, detailing the accident, injuries, treatment, and financial impact, which can compel the insurance company to consider a fair settlement.

However, it’s important to be aware that insurance companies often adopt a defensive stance. Their default approach may be to deny claims or, when liability is clear, attempt to minimize their payout through delay and other tactics.

Even when you’ve done everything right, it’s possible, if not likely, that the insurance company will not make a fair settlement offer immediately.

Therefore, patience, persistence, and professional guidance are often necessary in navigating these complex negotiations.

What is a Demand Letter?

A demand letter is a formal document that is typically sent by one party to another, requesting some form of restitution or action.

In the context of personal injury law, a demand letter is often sent by an injured party (or their representative) to an insurance company, outlining the details of an accident, the injuries sustained, the treatment received, and the associated costs.

The letter serves as a formal request for compensation from the insurance company.

Demand letters can be used in various scenarios, not just in personal injury cases. They can be used in business disputes, for example, where one party may be seeking payment or other action from another party.

They can also be used in property disputes, employment disputes, and many other situations where one party believes they are owed something from another party.

The demand letter serves as formal notice to insurance carriers of the claim being made against them.

It outlines the claimant’s case in detail, providing the insurance company with the information they need to assess the claim.

This includes details of the accident, medical reports, evidence of financial losses, and any other relevant information.

In some situations, the demand letter can become an exhibit itself in future litigation.

This can occur if the insurance company acts in bad faith, for example, by denying a valid claim without a reasonable basis or failing to conduct a proper investigation into the claim.

In such cases, the demand letter can be used as evidence to demonstrate the insurance company’s knowledge of the claim and their subsequent actions.

It’s important to note that crafting an effective demand letter can be complex and requires a thorough understanding of the law and the specifics of the individual case.

Therefore, it’s often beneficial to seek professional help when drafting a demand letter. This ensures that all relevant information is included and that the letter is structured in a way that maximizes its impact.

The Role of Demand Letters in Car Accidents

In the aftermath of a car accident (or any personal injury), a demand letter is often the first step in seeking compensation.

It outlines the circumstances of the accident, the injuries sustained, and the financial impact.

The demand letter sets the stage for negotiations with the insurance company, and its effectiveness can significantly influence the outcome of the claim.

Crafting a Demand Letter: Key Components

The approach to writing a demand letter is not one-size-fits-all; it varies significantly based on the facts and nature of the case.

Factors such as whether liability is contested or clear-cut, the recipient of the demand (be it an insurance company, an individual, or a corporation), and the claimant’s objectives all influence the structure and tone of the letter.

For instance, if a quick resolution is desired, the letter might be more conciliatory, offering a compromise to expedite settlement.

Conversely, if the goal is to maximize the value of the claim, regardless of the time it may take, the letter might be more assertive, detailing every aspect of the claim to justify a higher compensation.

Other factors, such as the severity of injuries, the clarity of evidence, and the jurisdiction’s specific laws, also play a crucial role in shaping the demand letter. Therefore, each demand letter is unique and should be tailored to the specifics of the case at hand.

While the substance of what is included in the demand will vary, generally the demand should include the following sections:

Introduction

This section identifies the sender and the recipient of the letter. For example, “Dear [Insurance Company], I am writing on behalf of my client, [Client’s Name], regarding the car accident that occurred on [Date].”

Or if you are representing yourself it might look more like this:

Dear [Adjuster’s Name],

I am writing to formally present my demand for compensation following the accident that occurred on [Date of Accident], in which I was involved and suffered injuries. I am representing myself in this matter, and I believe that your insured, [At-Fault Party’s Name], is responsible for the accident and the subsequent damages I have incurred.

Please treat this letter as my formal demand for compensation.

Description of the Accident

Here, you provide a detailed account of the accident, including the date, location, and any relevant circumstances. For example: “On [Date], at approximately [Time], my client was driving southbound on [Street Name] when your insured, [At-Fault Driver’s Name], failed to stop at a red light and collided with my client’s vehicle.”

In more complex cases, a more detailed description of the accident may be required.

Including additional detail may also signal to the insurance carrier or other party that your theory of liability, which follows the description, is more likely than their purported defense.

For example:

On August 1, 2024, at approximately 5:30 PM, I was driving my vehicle, a 2020 Honda Accord, westbound on Kennedy Boulevard in Tampa, Florida. As I approached the intersection with Hyde Park Avenue, the traffic light for my direction was green, indicating my right of way.

Simultaneously, a blue 2018 Ford F-150, driven by your insured, was traveling northbound on Hyde Park Avenue. Despite the traffic light for Hyde Park Avenue being red, your insured failed to stop and entered the intersection. In an attempt to avoid a collision, I applied my brakes and swerved to the right. However, the Ford F-150 collided with the driver’s side of my vehicle.

Following this initial impact, the momentum from the collision forced my vehicle into the southbound lane of Hyde Park Avenue, where it was struck again on the passenger side by a southbound 2019 Toyota Camry.

The entire sequence of events unfolded in a matter of seconds, leaving me with no safe or effective means of avoiding the collisions. The Tampa Police Department responded to the scene, and their report corroborates my account of the incident. The report also includes statements from several eyewitnesses who confirm that your insured ran the red light, thereby causing the accident.

Liability and Fault

This section explains why the recipient of the letter (or their insured) is at fault for the accident. For example, “Based on the police report and witness statements, it is clear that your insured is at fault for the accident.”

It is often helpful to include these reports as attachments to your demand, particularly when attempting to quickly resolve the matter.

Damages Incurred

This part lists the injuries and damages you have suffered as a result of the accident. For example, “As a result of the accident, my client suffered a broken collarbone and whiplash, requiring extensive medical treatment and physical therapy.”

In addition to listing the injuries incurred you will likely want to reference the cost of the damages by itemizing medical bills, lost wages, and the cost of property which was damaged, destroyed, or otherwise lost.

If a permanent injury was suffered you may estimate the cost of medical care to be expected in the future, lost or diminished future earnings, or even the loss of companionship if a loved one was lost.

Demand for Compensation

Finally, this section specifies the amount you are seeking in compensation. Calculating the full and final extent of your damages is a crucial step in drafting a demand letter for a personal injury claim.

The importance of this comprehensive calculation lies in its influence on the settlement negotiation.

The figure you present in your demand letter essentially sets the baseline for these negotiations. If you underestimate your damages, you risk receiving a settlement that doesn’t fully cover your losses.

Conversely, an overestimate might prolong the negotiation process or cause the other party to refuse to negotiate if the insurance company views the demand as unreasonable.

If the other party accepts the demand, it typically results in a settlement agreement.

This agreement, once signed, effectively ends the case. It’s a legally binding contract where the injured party agrees to accept the specified compensation in return for releasing the at-fault party from further liability.

Therefore, it’s essential to ensure that the demand accurately reflects all damages before agreeing to a settlement.

Here is an example of how you may make the demand:

Given the extent of my injuries and the associated costs, I am seeking compensation for my damages. To date, my medical bills amount to $15,000.

In addition, my doctor anticipates that I will require further treatment, which is estimated to cost an additional $5,000. Due to my injuries, I have been unable to work, resulting in lost wages of $10,000.

Furthermore, the pain and suffering I have endured as a result of this accident cannot be overlooked, for which I am attributing a value of $20,000. Therefore, taking into account all these factors, I am demanding a total compensation of $50,000.

I hope that we can resolve this matter promptly and fairly. If I do not receive a response to this demand within 30 days, I will pursue further legal action.

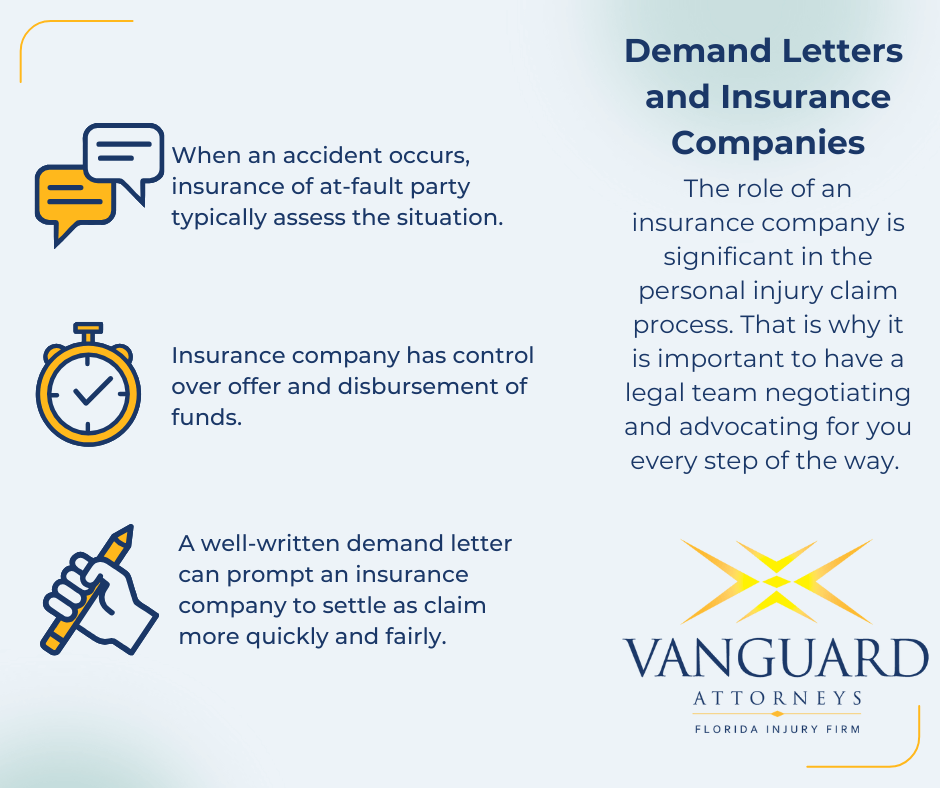

Demand Letters and Insurance Companies

Insurance companies play a significant role in personal injury claims, primarily because they have control over many aspects of the claim process.

When an accident occurs, the insurance company of the at-fault party is typically the one that assesses the situation, determines the liability, and decides on the settlement amount.

They have the authority to negotiate settlements and can decide whether to settle a claim out of court or proceed to litigation.

The insurance company also has control over the disbursement of funds. They decide how much to offer for various damages such as medical expenses, property damage, lost wages, and pain and suffering. This is why they are often the main point of contact for personal injury claims.

In essence, the control that insurance companies have over the claim process underscores their significant role in personal injury claims. It’s a complex system with many moving parts, and the insurance company is at the center of it all.

A well-written demand letter can prompt an insurance company to settle a claim more quickly and fairly. However, it’s important to be prepared for possible pushback or negotiation from the insurance company.

Florida Legal Requirements

In Florida, certain laws and regulations may affect how demand letters are written and handled. With recent changes to Florida law and more changes on the horizon, it is important for Floridians to consult with a lawyer before sending a demand letter in all but the simplest circumstances where damages may be minimal.

A well-meaning injury victim trying to quickly settle their claim for fair compensation may find themselves hurting their own interests by making a demand, particularly if the adverse party is a savvy insurance company.

Case Study: Crafting a Demand Letter After a Car Accident

The Accident

On August 1, 2024, Pete Mitchell was driving home from work on a clear, sunny day in Tampa, Florida. As he was crossing an intersection at Kennedy Boulevard and Hyde Park Avenue, another driver, who was texting while driving, ran a red light and collided with Pete’s car. Pete suffered a broken arm and whiplash as a result of the accident.

Medical Treatment

Pete was rushed to the hospital where he received immediate medical attention. His broken arm required surgery and he had to undergo several weeks of physical therapy for his whiplash. The total cost of his medical treatment amounted to $20,000.

The Demand Letter

Pete crafted a demand letter to Progressive, the at-fault driver’s insurance company. Here’s how he structured his letter:

Dear Progressive,

I am writing on behalf of myself, Pete Mitchell, regarding the car accident that occurred on August 1, 2024. On that day, at approximately 4:30 PM, I was driving southbound on Kennedy Boulevard when your insured, Mr. Kazansky, failed to stop at a red light at Hyde Park Avenue and collided with my vehicle.

Based on the police report, witness statements, and the fact that your insured was ticketed for texting while driving, it is clear that your insured is at fault for the accident. As a result of the accident, I suffered a broken arm and whiplash. I required surgery for my broken arm and several weeks of physical therapy for my whiplash. The total cost of my medical treatment amounted to $20,000.

Enclosed you will find copies of my medical bills and employment records documenting my lost earnings.

Considering the medical expenses, loss of earnings due to time off work, and pain and suffering endured, I am seeking compensation in the amount of $75,000.

This demand will remain open for 30 days.

Sincerely, Pete Mitchell

Pete sent his demand letter via certified mail to ensure it was received by Progressive. He also kept a copy of the letter for his records.

The Settlement

Two weeks later Progressive sent a letter offering Pete $15,000. He would continue negotiating with Progressive before ultimately settling for $50,000 on the condition her released Mr. Kazansky from any future liability related to the crash.

This case study illustrates the importance of a well-crafted demand letter in personal injury claims. It provides a structured way to present your case to an insurance company and can significantly influence the outcome of your claim.

Will the Insurance Company Offer a Fair Settlement?

No. Insurance companies are generally for-profit institutions where adjusters report to management who reports to executives who report to owners. All along the way they are judged by one standard how much money they make for the company.

Their job is to take in as much money as possible and hold onto that money as long as possible while paying out as little as possible on claims.

So generally speaking unless the adjuster (insurance company) is concerned that a claimant will initiate a lawsuit wait out the insurance company and ultimately win a big verdict, they will typically undervalue the claim and make offers substantially lower than the true value of the injuries.

Therefore when you are considering making a demand for your injuries, particularly when it involves an insurance company, you should first consult with an attorney.

Our attorneys are available for free consultations at your convenience, call today to protect your rights!